European Union Banking Sector Statistics (2013)

Pagano, Andrea; Di Girolamo, Francesca (2026): European Union Banking Sector Statistics (2013). European Commission, Joint Research Centre [Dataset] doi: 10.2905/JRC.TSF5F20 PID: http://data.europa.eu/89h/jrc-eubss-eubss-2013

European Union Banking Sector Statistics (2013) - Excel format: EU 28 banking sector sample aggregate by countries. Sample Statistics. JRC elaboration on Bankscope data.

European Union Banking Sector Statistics (2013) - Excel format: EU 28 banking sector population aggregate by countries. Population statistics. Main data sources are Eurosta for GDP; BIS for banks' exposusres; ECB for Total Assets. JRC survey for covered and eligible deposits.

Information about main source for EU 28 banking sector sample.

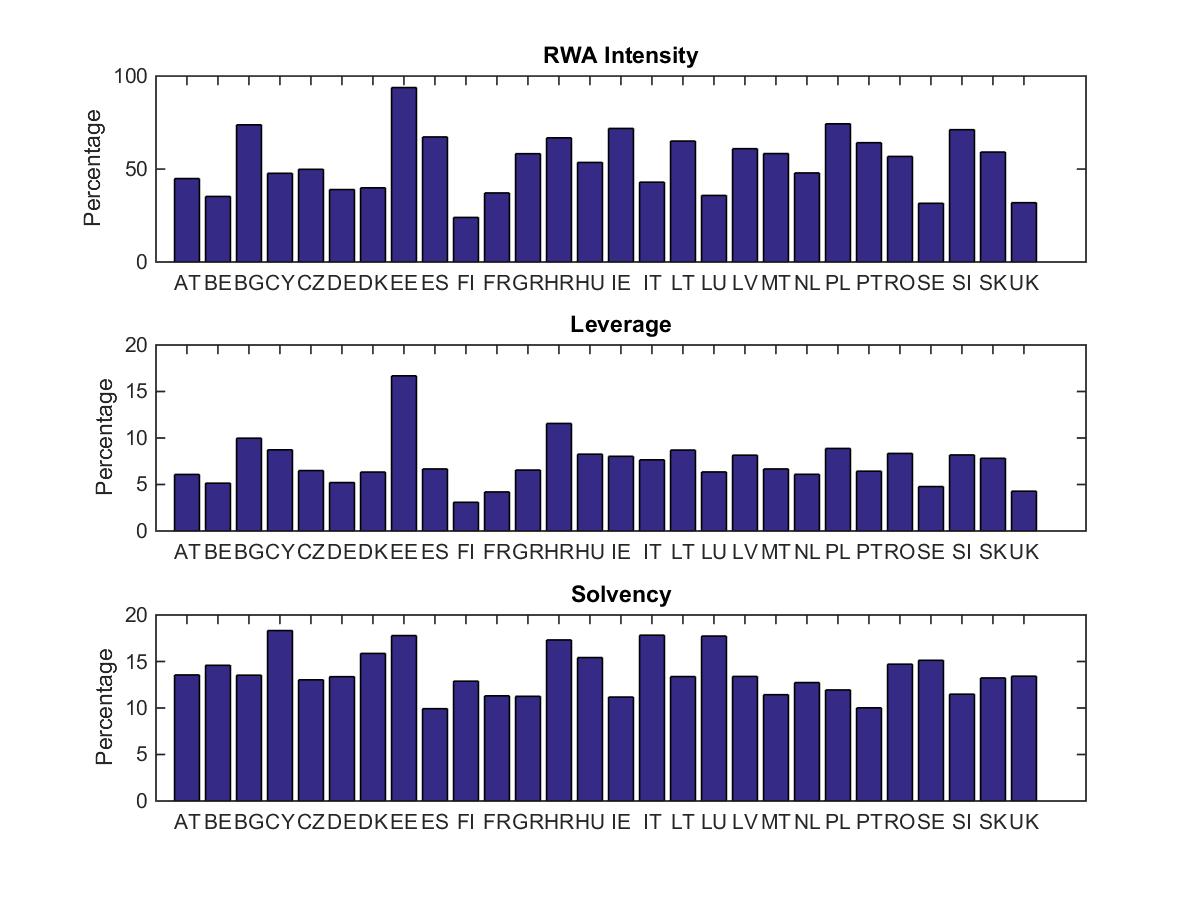

Graph showing three key drivers associated to banks' default probability. Sample aggregates by countries.

The latest economic and financial crisis has shown how quickly vulnerabilities on the financial side of the economy can turn into a strong deterioration of public accounts, thus highlighting the importance to monitor fiscal risks arising outside the realm of public finances. This is particularly the case for the building up of risks in the banking sector, due to its central role in financial stability. In this spirit, this paper presents banking stress-test scenarios for public debt projections based on SYMBOL, a Monte Carlo micro-simulation model that allows obtaining losses from simulated bank defaults, using actual bank balance-sheet information. The estimated bank losses are used to assess the size of the potential impact on government deficit and gross public debt that feed into a debt projection model, allowing drawing conclusions in terms of projected public debt dynamics. The methodology for the stress tests proposed here has three major advantages. First, it allows distinguishing between simulated bank losses and bank recapitalisation needs (particularly relevant in that public funds used to cover the latter could be recouped later by selling the financial assets acquired). Secondly, through the use of bank-level balance-sheet data, countryspecific

features of national banking systems are accounted for, while remaining within a common conceptual framework. Thirdly, the approach allows reflecting in the designed stress tests the institutional changes (bail-in, elements of Basel III, the resolution fund) along the path leading to the full implementation of the banking union legislation. Results for a selected group of EU countries are presented in the paper based on end-2013 bank balance-sheet data.

The report demonstrates that the contingent liabilities associated with efforts to limit the externalities stemming from the European banking sector are substantially decreasing as a result of new regulation. Noting that the implied shifting of losses from taxpayers to bank creditors is desirable, the report recognises that losses do not disappear. It discusses the issue of where bank recovery or resolution bail-in losses may go. It underlines that the sectoral allocation of losses matters, but concludes that our understanding needs to be further developed and that more transparency about the structure of bank creditors would be desirable. Increasing transparency in this regard would, among other things, help assure policy makers that the new tools available can be used effectively and smoothly in actual practice. Also, raising awareness of investors in bail-inable bank debt about the associated risks should enhance the credibility of the bail-in framework.

| From date | To date |

|---|---|

| 2013-01-01 | 2013-12-31 |

{kind=link}